")

")

In Diana Chacón Consulting’s latest blog, our senior consultant Maria Angélica Campoverde shares a personal account that many of us recognize: the relentless “one-click” credit offer.

By blending her experience as a consumer with an analysis of Ecuadorian regulation, Angelica brings a case study on aggressive marketing and makes us question whether “convenience” is becoming a cover for over-indebtedness?

Read the full analysis below:

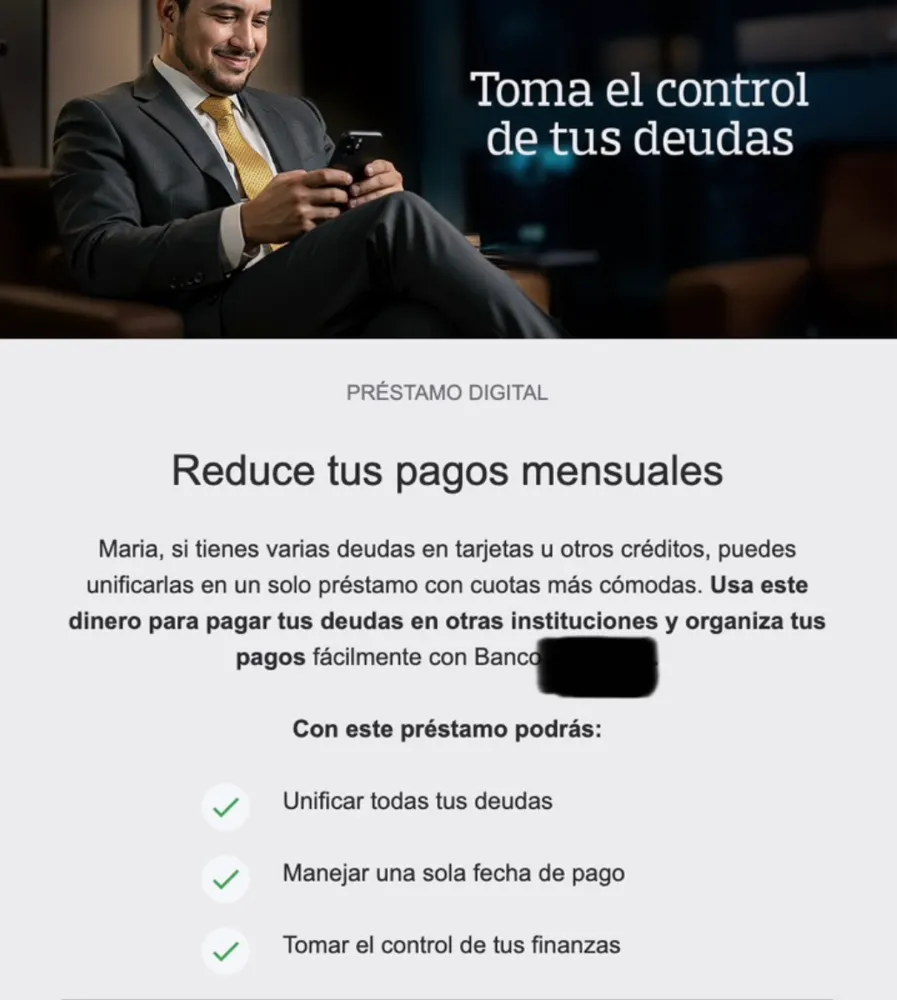

A few weeks ago, I received an email from my bank stating:

“pay less on your debts, take control of them, reduce your monthly payments, consolidate your loans, and manage a single payment date.”

Original message of the SMS in Spanish

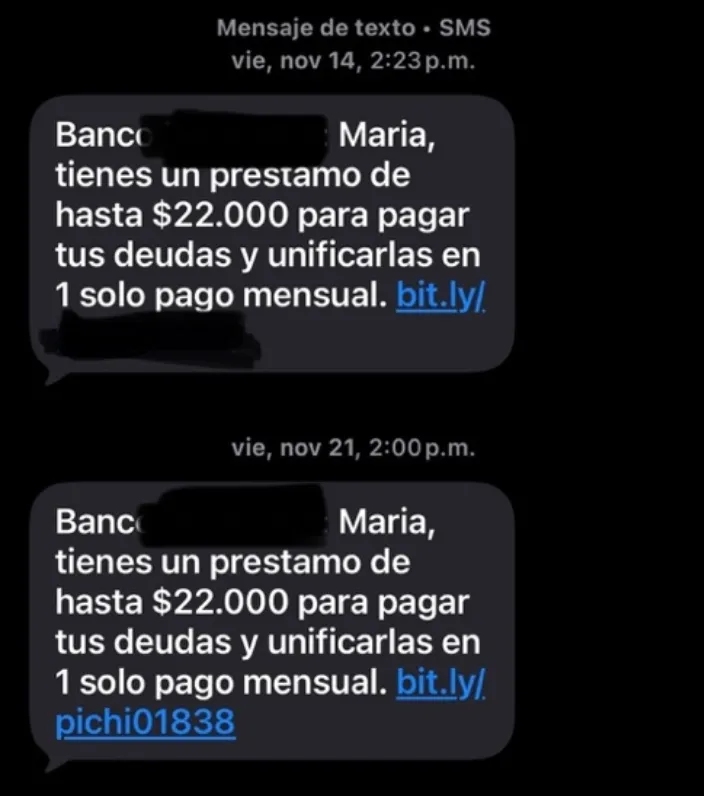

The email went straight to the trash, and I continued with my day. I gave it little thought. However, five days later I received a text message with a similar content, but this time the offer contained a pre-approved amount:

“(…) and you have a pre-approved loan of up to USD 22,000 to pay off your debts and consolidate them into a single monthly payment.”

A week later, another message arrived. As if that were not enough, a loan officer called me on a Saturday morning to convey exactly the same offer.

Original message of the SMS in Spanish

The “Installment Illusion”

At that point, my curiosity was piqued, and I asked how the pre-qualification process worked and how long it would take to know whether the loan was approved. His answer was surprising:

“if you say yes, right now, you log into online banking, click once to accept the loan, and the funds are credited immediately to your account”.

Then, I asked the most fundamental question in consumer finance: what is the total cost of credit? The officer couldn’t answer. He didn’t disclose the annual percentage rate (APR), whether the rate was fixed or variable, or the total amount I would pay over the life of the loan. He stayed anchored to a single, seductive figure:

“Comfortable monthly installments of USD 400.”

This is what experts call the “installment illusion”, focusing the consumer on monthly “affordability” to obscure the long-term cost of debt.

Upon reviewing my inbox more carefully, I noticed that I also had two similar unsolicited messages from banks with which I am not even a customer.

Normalizing the Abnormal in Ecuador

All of this led me to reflect on financial regulation and supervision in Ecuador, where I live and where these practices occurred. Is it really lawful for financial institutions to promote unsolicited loans that may lead to over-indebtedness in an economy as fragile as Ecuador’s? We have normalized the abnormal.

El crédito puede ser una herramienta muy útil. Puede ayudar a enfrentar emergencias, estudiar, emprender o mejorar la calidad de vida. Pero cuando se ofrece bajo parámetros irresponsables, sin evaluar si la persona realmente puede pagarlo, el créditodeja de ser una solución y se convierte en un problema.

This concern is neither new nor isolated. At the international level, The World Bank Group, in its Good Practices for Financial Consumer Protection, has been clear in stating that the expansion of access to financial services is positive only when accompanied by clear consumer protection rules. Credit providers have a duty to act fairly, transparently, and responsibly, ensuring that consumers fully understand the terms of the product and its real financial impact on their economic situation. It is an essential practice that consumers be clearly and in advance informed of the total cost of credit, interest, fees, and charges, and that there be a reasonable assessment of their repayment capacity.

Along the same lines, the Basel Committee on Banking Supervision, whose principles guide banking supervision globally, including in Ecuador, has emphasized that consumer protection must be an integral part of any financial inclusion policy. The logic is simple: expanding access to credit without adequate safeguards does not create inclusion, but rather transfers risk to individuals and households. Accordingly, BIS’s Basel Committee on Banking Supervision incorporates disclosure and transparency as core principles of effective banking supervision, precisely to prevent consumers from making decisions without fully understanding the obligations they are assuming.

The Tactic of “Push” Credit

When we analyze these practices against international best practices, three pillars of protection are consistently violated:

- Avoidance of aggressive advertising: Multiple unsolicited contacts (SMS, email, calls) constitute aggressive behavior designed to induce impulsive decision-making.

- Repayment capacity assessment: Offering a loan based on the knowledge that a client is already indebted, without a fresh cash-flow analysis, is a failure of the bank’s due diligence.

- Full disclosure: Presenting a loan as “relief” without disclosing the APR or the total cost of the loan is a form of misleading advertising that exploits cognitive biases.

These credit offers intensify during periods of high and often unnecessary spending, such as Black Friday, Christmas, and year-end travels. All of this is accompanied by a common denominator: a profound lack of financial education. In this context, practices that are presented as financial relief can become mechanisms that deepen household indebtedness.

The Regulatory Paradox

In Ecuador the Codification of the Regulations of the Superintendencia de Bancos Ec. provide a theoretical framework for protection through an entire chapter on the protection of financial consumers. It recognizes the right to receive complete information, including the characteristics, conditions, risks, and costs of financial products, and establishes that the provision of services must be aligned with best practices and with the principles of the Basel Committee.

However, it is striking that the regulation, when addressing the so-called “sound practices,” places a significant burden on the financial consumer. Article 26 establishes as obligations of users that they ensure the entity is authorized, actively inform themselves about product conditions, demand verbal and written explanations, review contracts, identify complaint channels, and monitor the information received.

In practice, this starts from an unrealistic premise: that the financial consumer has the technical knowledge and the capacity to challenge complex financial products, even when they are offered in an immediate, persistent, and simplified manner, with a single click. This logic ignores the information asymmetry, which occurs when one party in a transaction has more or better relevant information than the other, creating an imbalance of power that can lead to unfair deals or exploitation. Therefore, international standards place the primary burden of transparency and responsibility in the financial institution, not with the consumer.

This is not about denying that consumers have responsibilities. They do, and fostering an informed attitude is positive and necessary. But when credit is extended without explaining any details about its price, and without adequately assessing repayment capacity, requiring the consumer to “inquire” or “ask better questions” ultimately weakens the protection that the regulation claims to guarantee.

El crédito debe ser una decisión consciente e informada, no un impulso generado por la publicidad.

El crédito puede abrir puertas, pero también puede cerrarlas si se utiliza sin responsabilidad.

En el último blog de Diana Chacón Consulting, nuestra consultora senior, Maria Angélica Campoverde, comparte un relato personal que muchos reconocemos: la incesante oferta de crédito “a un solo clic”.

Al combinar su experiencia como consumidora con un análisis de la regulación ecuatoriana, Angélica presenta un caso práctico de marketing agresivo y nos hace preguntarnos si la “conveniencia” se está convirtiendo en una excusa para el sobreendeudamiento.

Lea el análisis completo a continuación:

Hace pocas semanas recibí un correo electrónico de mi banco en el que se me indicaba:

“paga menos por tus deudas, toma el control de tus deudas, reduce tus pagos mensuales, unifica tus deudas y maneja una sola fecha de pago”

El correo fue directamente a la papelera y continué con mi día. No le di mayor importancia. Sin embargo, cinco días después recibí un mensaje de texto con un contenido parecido, esta vez indicando una cantidad específica pre-calificada:

“tienes un préstamo aprobado de hasta USD 22.000 para pagar tus deudas y unificarlas en un solo pago mensual”

Una semana después, llegó otro mensaje similar. Como si no fuera suficiente, un asesor de crédito me llamó un sábado por la mañana para transmitirme exactamente la misma oferta.

La “Ilusión De Las Cuotas”

En ese momento sentí curiosidad y le pregunté cómo se realizaba la precalificación y cuánto tiempo tomaría saber si efectivamente me otorgaban el crédito. Su respuesta fue sorprendente:

“si usted me dice que sí, en este momento entra a la banca electrónica, hace un clic aceptando el prestamo y el dinero se acredita inmediatamente en su cuenta”.

Entonces le hice la pregunta más fundamental en finanzas de consumo: ¿cuál es el costo total del crédito?. La única respuesta que obtuve fue que tendría

“Comfortable monthly installments of USD 400.”

El asesor no pudo explicarme la tasa efectiva anual, si la tasa era fija o variable, ni el valor total del crédito. Ahí terminó la interacción.

Esto es lo que los expertos llaman la “ilusión de las cuotas”, que centra al consumidor en la “asequibilidad” mensual para ocultar el coste a largo plazo de la deuda.

Al revisar mi correo con más detenimiento, noté que tenía además dos mensajes similares de bancos de los cuales ni siquiera soy cliente.

Normalizing the Abnormal in Ecuador

Todo esto me llevó a reflexionar sobre la regulación financiera en Ecuador, lugar donde vivo y donde estas prácticas ocurrieron. ¿Es realmente legal que las insituciones financieras promuevan prestamos no solicitados, que pueden llevar al sobreendeudamiento de las personas en una economía tan frágil como la Ecuatoriana? Hemos normalizado lo anormal.

Credit can be a very useful tool. It can help address emergencies, finance education, start a business, and overall, improve quality of life. But when it is offered under irresponsible parameters, without assessing whether a consumer can actually repay it, credit ceases to be a solution and becomes a problem.

Esta preocupación no es nueva ni aislada. A nivel internacional, el Banco Mundial, en su Manual de Buenas Prácticas para la Protección del Consumidor Financiero, ha sido claro en señalar que la expansión del acceso a servicios financieros solo es positiva cuando va acompañada de reglas claras de protección al consumidor. Los proveedores de crédito tienen la obligación de actuar de forma justa, transparente y responsable, asegurando que los consumidores comprendan plenamente los términos del producto y el impacto financiero real que este tendrá sobre su situación económica. En particular, es una práctica esencial que el consumidor conozca, de forma clara y previa, el costo total del crédito: intereses, comisiones y cargos, y que exista una evaluación razonable de su capacidad de pago.

En la misma línea, el Comité de Supervisión Bancaria de Basilea, cuyos principios guían la supervisión bancaria a nivel global incluyendo la ecuatoriana, ha señalado que la protección del consumidor debe formar parte integral de cualquier política de inclusión financiera. La lógica es simple: ampliar el acceso al crédito sin salvaguardias adecuadas no genera inclusión, sino transferencia de riesgos a las personas y a los hogares. Por ello, Basilea incorpora la divulgación y la transparencia como principios esenciales de una supervisión bancaria efectiva, justamente para evitar que los consumidores tomen decisiones sin comprender plenamente las obligaciones que están asumiendo.

La táctica del crédito “push”

Al comparar estas prácticas con las mejores prácticas internacionales, se vulneran sistemáticamente tres pilares de protección:

- Evitar la publicidad agresiva: Los contactos no solicitados (SMS, correo electrónico, llamadas) constituyen un comportamiento agresivo diseñado para inducir la toma de decisiones impulsivas.

- Evaluación de la capacidad de pago: Ofrecer un préstamo basándose en el conocimiento de que un cliente ya está endeudado, sin un nuevo análisis del flujo de caja, constituye una falta de diligencia debida por parte del banco.

- Divulgación completa: Presentar un préstamo como “alivio” sin revelar la TAE ni el coste total del préstamo es una forma de publicidad engañosa que explota sesgos cognitivos.

Estas ofertas de crédito se intensifican durante periodos de gasto elevado y a menudo innecesario, como el Black Friday, la Navidad y los viajes de fin de año. Todo esto va acompañado de un denominador común: una profunda falta de educación financiera. En este contexto, las prácticas que se presentan como alivio financiero pueden convertirse en mecanismos que profundizan el endeudamiento de los hogares.

La Paradoja Regulatoria

En Ecuador, existe un capítulo completo sobre la protección y defensa de los derechos del consumidor financiero de las entidades públicas y privadas del sistema financiero nacional en la Codificación de las Normas de la Superintendencia de Bancos Ec.. Se reconoce el derecho a recibir información completa, que incluya características, condiciones, riesgos y costos del producto financiero, y se establece que la prestación de servicios debe alinearse con las mejores prácticas y con los principios del Comité de Basilea.

Sin embargo, resulta llamativo que la normativa, al regular las denominadas “sanas prácticas”, traslade una carga importante al propio consumidor financiero. El artículo 26 establece como obligaciones del usuario cerciorarse de que la entidad esté autorizada, informarse activamente sobre las condiciones del producto, exigir explicaciones verbales y escritas, revisar contratos, identificar canales de reclamo y controlar la información recibida.

En la práctica, esto supone partir de una premisa poco realista: que el consumidor financiero tiene el conocimiento técnico y la capacidad de cuestionar productos financieros complejos, incluso cuando estos se le ofrecen de forma inmediata, insistente y simplificada, con un solo clic. Esta lógica ignora la asimetría de información, que ocurre cuando una de las partes en una transacción tiene más o mejor información relevante que la otra, creando un desequilibrio de poder que puede conducir a acuerdos injustos o explotación. Sin embargo, los estándares internacionales, recomiendan que la carga principal de transparencia y responsabilidad recaiga en la entidad financiera, no en el cliente.

No se trata de negar que el consumidor tenga responsabilidades. Las tiene, y es positivo y necesario fomentar una actitud informada. Pero cuando un crédito se coloca sin explicar el costo total y sin evaluar adecuadamente la capacidad de pago, exigir que el consumidor “indague” o “pregunte mejor” termina debilitando la protección que la norma dice garantizar.

Credit should be a conscious and informed decision, not an impulse driven by advertising.

Credit can open doors, but it can also close them ifused irresponsibly.

DO SUCH OFFERS ALSO REACH YOUR INBOXES AND CELL PHONES?